Complete Guide to Singapore Government Securities (SGS Bonds)

Ever heard of the famous quote by Warren Buffett? “If you don’t find a way to make money while you sleep, you will work until you die.”

This is perfectly true, especially for many of us who aren’t so lucky to be born with a silver spoon.

One way to make money even while we are asleep is by investing. But if we are new to the world of investing and do not want to dive into the risk before even seeing the returns immediately, how should we begin?

Why not consider SGS bonds to start and diversify your investment portfolio?

What are SGS?

SGS bonds are debt securities issued by the Singapore government that allow you to receive a fixed, steady income twice a year (every 6 months) starting from the month of bond purchase until the bond matures.

Upon maturity of the bond, you receive the principal sum – your initial investment back.

It works similarly to any other type of bond, so I highly recommend reading our guide to bond investing in Singapore if you haven’t yet.

The main difference between the SGS and typical bonds is that it is a safe, long-term investment issued by the Monetary Authority of Singapore (MAS) on behalf of the government of Singapore.

There are three kinds of MAS-issued securities, also known as the Singapore Government Securities:

- SGS Bonds

- Treasury Bills (SGS T-Bills)

- Singapore Savings Bonds (SSB)

SGS bonds were first issued in 1998 by the MAS as part of the government’s efforts to promote Singapore as an international debt hub by offering banks risk-free assets in their liquid asset portfolios.

In simpler terms, when you make SGS bonds purchases, you are loaning your money to the Singapore government, and in return, you will receive interest depending on the amount you put in.

How does SGS work?

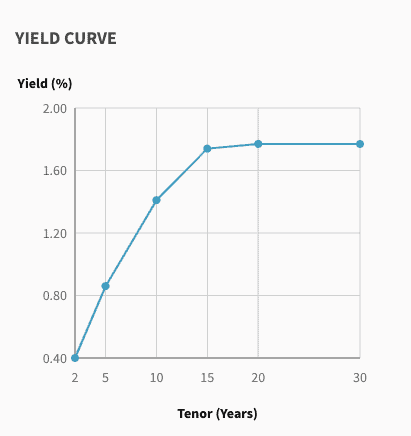

SGS bonds are long term bonds with varying maturity periods ranging from 2,5,10,15,20, or 30 years. When you hold SGS bonds, you receive a fixed sum of interest every 6 months until the bond matures in the form of coupon payments.

Based on previous data, yields vary from 0.41% pa for 2 years to 1.82% pa for 30 years. (Refer to the graph below.)

SGS Bond Yield Curve, Monetary Authority of Singapore

Here’s an example that will help you understand better.

Suppose you decide to purchase $1,000 of SGS bonds, and the interest rate is 1%, then you will receive $10 in the form of two $5 coupon payments twice a year (every six months) until the bond matures.

The longer the maturity period, the higher the interest received. Do also note that the interest rates will vary for the different SGS bonds offered.

Singapore Savings Bonds (SSB) versus Singapore Government Securities (SGS). What’s the difference?

Below is a comparison chart of the differences between SGS and SSBs, which might be useful for your consideration.

| SSB | SGS | |

| Investment Duration | 10 Years | 2,5,10,16,20,30 Years |

| Payouts | 2 payouts in a year (every 6 months) | 2 payouts in a year (every 6 months) |

| Minimum investment | $500 | $1,000 |

| Maximum investment | $200,000 | No limit |

| Risk | Lower risk:

You are guaranteed par value when selling bonds. You will receive your sum invested back when the bond matures or when you exit. |

Higher risk:

The amount you received might be higher or lower when you sell your bonds. |

| Flexibility of Exit | Exit anytime without penalties. | Cannot be redeemed early. |

| Interest rates | Rates are fixed and published by MAS every month | Rates are determined by auction. |

| Mode of purchase and sale | Via online banking service or ATM paid only using cash. | Traded in open stock or bond markets using cash and or CPF. |

Advantages of SGS

Below is a list of advantages of the SGS.

Fully backed by the Singapore Government.

Therefore it is more reliable and stable with lesser risk than company-issued bonds and the stock market. This will be a sound and safe way to diversify your investment portfolio, as you are very likely to receive your initial investment capital back.

Earn regular interest

You will receive payouts twice a year from the month you purchase the bond till the day your bond reaches its maturity period. The payouts are more stable and fixed as compared to other investments where the returns are not guaranteed.

Furthermore, the longer you hold your bond, the higher the returns. As you hold your bond, the interest paid out to you steadily increases until maturity.

Capital Gains

You might be able to purchase bonds below their par value in the secondary market. When sold or upon maturity, you earn the difference as profit on top of the annual yield received.

This is another plus point why you should consider SGS bonds as compared to SSBs. Besides its stability, you have chances to earn more than the interest rates given.

Low Investment Capital Needed

The SGS requires an affordable minimum investment sum of $1,000. Unlike other investments and certain stocks, you don’t need a considerable sum to get started.

Besides, SGS bonds can be a way for you to put some of your savings in as it offers you a higher interest rate than your savings account.

Invest with Cash, CPF, or SRS!

It can be bought with cash, Central Provident Fund (CPF), or your Supplementary Retirement Scheme (SRS).

Unlike SSBs, which only allow cash investments, the SGS works your CPF and SRS monies, preparing you for a more comfortable retirement.

Tax Exemptions

Individuals who invest in SGS bonds can receive tax exemption on the amount invested in SGS bonds.

This means that you don’t have to worry about being taxed for your investments in SGS bonds, more value in your pocket!

A good consideration point when you’re planning your taxes.

Disadvantages of SGS

Below is a list of disadvantages of the SGS.

Low ROI

The SGS has lower returns on investment than other assets such as stocks, unit trusts, REITs, and ETFs. Furthermore, the value of your returns may decrease due to inflation.

According to the Monetary Authority of Singapore (MAS), the yearly inflation rate is about 1.5%.

Assuming you get a 1.82% annualised interest over 10 years, you only earn 0.32% in interest! And that’s if the interest rates stay or remain below 1.5%.

If it gets higher, you’re essentially losing your money to inflation.

Long Maturity Period

SGS bonds take between 2 to 30 years to mature. For you to reap the total value, you’ll need to keep it in your portfolio longer or incur the opportunity costs involved.

Capital Loss

Although I mentioned capital gain as an advantage, this is essentially a double-edged sword.

If you need the money and sell it through the secondary markets, you could potentially lose out by selling below par value or the price you bought it for.

That’s why it’s always essential to make sure you have enough emergency funds and insurance coverage to protect your investments and your family.

Requires a CDP Account

A CDP account is required for the buying and selling of SGS Bonds. CDP accounts are only available to Singaporeans and permanent residents aged 18 and above.

This might not be a disadvantage to you if you already have or can qualify for one, but some might be affected by this requirement.

Who should get SGS?

Singapore government securities bonds are suitable for investors who

- Are new to investing.

- Do not want to take the risk that stocks and other investments hold but prefer higher interest rates than their savings accounts.

- Have safe and regular interest payouts.

- Certain retirees due to their low-risk nature.

How to buy SGS?

You can buy SGS via primary markets or secondary markets.

Primary Market

Purchase of SGS from the primary market is made through an auction system, where anyone can participate.

All bids must be submitted through any one of the SGS Primary Dealers. The SGS Primary Dealers are mainly banking financial institutions in Singapore, listed below:

- Bank of America

- Barclays Bank

- Citibank

- Credit Suisse First Boston

- Deutsche Bank

- DBS Bank

- HSBC Bank

- OCBC Bank

- Royal Bank of Scotland

- Standard Chartered Bank

- UOB

It is rare to see retail investors investing in SGS via the primary market. The primary market is more suitable for big bidders like funds and companies due to the large trading volume these parties offer.

Nonetheless, you can still submit your bids at ATMs. You will be required to set up a CDP account as successful bids will be deposited in it.

Secondary Market

If you do not wish to go through the hassle of bidding and prefer more transparency by knowing what you are bidding for, the secondary market is a more straightforward and preferred option.

SGS bonds are listed on the Singapore Exchange (SGX) to be purchased just like stocks and shares and stored in your CDP account.

Trading SGS bonds on SGX will incur fees for transaction and brokerage. A list of SGS bonds available for trading can be found on the SGX webpage here.

Besides cash, you can use your CPF Ordinary and SA (Special Account) to make your SGS bonds purchase. You will also need a CPF Investment Scheme (CPFIS) account to buy and sell bonds with CPF monies.

How do you decide on which SGS bonds to invest in though?

You will have to conduct your research and due diligence before coming to a decision.

We suggest you analyse and access market data from sources such as investment broker’s platforms and the MAS bond calculator.

From these sources, you will have access to bonds previously issued by the government, original prices of initial coupon release, up-to-date closing prices on the secondary market, and forecasted yields you can potentially receive based on the secondary market.

Below are a few tips to look out for which can help you decide which SGS bonds to invest in.

The higher the yield, the better.

The most crucial factor to consider when investing is the profits you can get from it. SGS yield terms are quoted annually.

Annual yields are the actual returns received from your investments per year. A higher yield is beneficial on your end as it means you can receive higher profits.

Get bonds below par value for higher profits.

The maturity value of the bond is known as the par value. This is because upon maturity, you will receive the bond at par value.

For SGS bonds, the par value is expressed in multiples of $100.

If a bond is sold at $80, this is seen as a bond sold below par – below its face value. When you sell this bond at its face value, you will earn $20 on top of the coupon payments you receive.

Conversely, if a bond has a par value of $100, but you bought it at a higher price of $120, you will make a loss of $20.

Dirty versus Clean Price

This should be a term you should familiarise yourself with. The above terms are the accrued interest that buyers have to compensate the seller for the upcoming coupon disbursed by the bond.

When you trade bonds at a dirty price, you will receive higher accrued interest as the bonds are sold close to the payout date of the bond.

When you trade at a clean price, there won’t be any accrued interest. All trades in the secondary market will be quoted the dirty price, which needs to be paid in cash.

Conclusion

We hope you managed to get insightful and valuable information regarding SGS bonds.

The SGS bonds is a safe long-term investment product that offers beneficial properties that can’t be easily found in higher-risk investments such as stocks.

We strongly advise you to assess your investment objectives and do your due diligence before deciding on any investments.

If you would like advice on whether SGS bonds are for you or need someone to aid you in building a financial portfolio customised just for you, talk to an unbiased financial advisor.

References

https://www.mas.gov.sg/bonds-and-bills/Singapore-Government-Bonds-Information-for-Individuals

https://www.dbs.com.sg/personal/ibanking/faq/sgsbond.page

https://www.ocbc.com/personal-banking/investments/singapore-government-securities

https://secure.fundsupermart.com/fsm/article/view/1227/s-pore-govt-bonds-in-a-nutshell

source https://singaporefinancialplanners.com/blog/singapore-government-securities-sgs/

Comments

Post a Comment